“I believe AWS is one of those dreamy business offerings that can be serving customers and earning financial returns for many years into the future. Why am I optimistic? For one thing, the size of the opportunity is big, ultimately encompassing global spend on servers, networking, datacenters, infrastructure software, databases, data warehouses, and more. Similar to the way I think about Amazon retail, for all practical purposes, I believe AWS is market-size unconstrained.”

– Jeff Bezos, 2014 Annual Letter to Shareholders

Background:

Since the summer is clearly over and it has recently started snowing here in Toronto, I’ve been more in the mood to write about another investment idea. In general I’ve been finding more interesting names to potentially short than go long in the US. I don’t believe I’m a great short seller. In fact I think it’s probably the hardest skill to master in this business, and making money consistently with an absolute return mandate and high risk-adjusted returns is extremely difficult. For now I view it more as an intellectual exercise which should augment my analytical skills until it has become apparent I’ve mastered the art of short selling. In general my view on short selling is that it’s a relative return business, and concentrated positions are not justified unless one believes the idea is more attractive than an idea on the long side; even if that were the case, due the leveraged nature of short selling, the vast majority of positions should always be sized smaller relative to long ideas. Just my 2 cents.

Moving on, I think some interesting long opportunities have been developing across the “large-cap information technology/media growth conglomerate” space.[i] I believe that some of these “conglomerates”, if I may call them that, have a dominant existing core business which generates relatively predictable cash flows; however, due to limited financial disclosure, they each also possess extremely valuable, but largely hidden growth assets which I believe have largely been under-appreciated or misunderstood by the market. Some notable examples include Google’s intention to reorganize its various business units into the “Alphabets”, which should provide increased financial disclosure to one of the most valuable assets in all of media – YouTube – or Facebook’s largely under-monetized social media portfolio which include hyper-growth assets such as Instagram, and private messaging apps such as FB Messenger and WhatsApp; did I also mention that Facebook owns one of the leading virtual/augmented reality businesses which could turn out to be a massive home-run investment? It is also worth noting that Google, alongside top VC firms Andreessen Horowitz and Kleiner Perkins have invested in the very secretive augmented reality start-up Magic Leap. It appears that the smartest money in the Valley are betting big on virtual reality as potentially the next major computing platform. One day soon, we could see a Minority Report-like future, and the potential applications of this technology certainly excite me! Even Microsoft stock which has had a largely uninspiring share price performance over the past decade or so, now looks kind of interesting from a sum-of-the-parts basis. Having looked rather closely at some of these names, if I had to buy one mega-cap US stock today, it would likely be Amazon.com. Put simply, Amazon is a collection of two high-growth, excellent businesses, run by a proven value creator and serial monopolist. In its Q1 filing this year, Amazon broke out some of the financials for its cloud computing platform, Amazon Web Services (AWS), which was the catalyst for me to take a deeper into this story. AWS is the undisputed industry leader in public cloud infrastructure services (IaaS) and will benefit from a massive multi-decade shift in IT resource spending from on-premise solutions to the public cloud. I believe it will be very likely that AWS will become the dominant public cloud computing platform of the 21st century, and we are only in the very first inning of this growth cycle.

A Trillion Dollar Valuation?

I believe the purchase of Amazon shares will be very rewarding for investors with a 5 year plus time horizon. My thesis on Amazon is centred around the AWS opportunity so the focus of this write-up will be on that segment; however, I do believe the retail segment is under-appreciated and materially undervalued on a standalone basis as well and I will further discuss this in detail below. In short, I believe the long-term profit opportunity for AWS is vastly under-appreciated by the market and that we are at a major industry inflection point in terms of the adoption of public cloud infrastructure services. My high conviction for this idea stems from my belief that AWS will be a much higher quality and valuable business than Amazon’s retail segment over time. AWS’ moat will only widen over time, and the total addressable market (TAM) that it is tackling is massive at conservatively $300bn+ and growing. In a couple of years, I think AWS’ standalone valuation (~$300bn by my estimate) will easily justify Amazon’s entire market capitalization today. Five years from now, both segments on a standalone basis should be worth well more than the entire current market cap. In fact, by 2020 and on a sum-of-the-parts basis, backing out the retail segment’s enterprise value at 20x 2020e EBIT or $470bn, we are getting paid to own the AWS segment for -5x EBIT and this segment alone could be worth more than $600bn or 2x Amazon’s current market-cap by 2020. The total future value from both segments plus the incremental free cash flow and working capital that will be generated over the next 4 years gives me a base case intrinsic value per share of $2,000 – $2,350 or a 4-year MoM of 3.0x-3.5x.

Key Points of Variant Perception

- I believe the market is largely under-estimating AWS’ long-term secular growth profile. According to Gartner, just the cloud infrastructure market alone will be worth around $17bn this year, and I think will likely grow at a 5-year 50% CAGR to nearly $130bn by 2020. AWS is currently a $8bn+ run-rate business with a ~47% share of this market and I expect this business will grow to well over $50bn or 6x larger over the next 5 years; this is well above the majority of Street estimates I’ve come across. But the IaaS market is just the tip of the iceberg. If we look at broader global IT spending across enterprises[ii] which includes platform and application software, we should be closer to at least a $1 trillion+ total addressable market (TAM) which makes AWS’ current market share de minimis; there is no reason for me to believe that AWS will not slowly expand into adjacent IT markets such as PaaS (of which they are already doing, successfully, I might add), and SaaS applications over the next 5-10 years. Very conservatively, I believe somewhere between 40%-50% of total IT spending could shift over to the cloud over the next decade or so, which would translate into a market opportunity of at least half a trillion for AWS. At the same time, enterprise adoption of infrastructure cloud services appears to be at a major inflection point, as AWS storage and computing usage rates are accelerating to near 100% growth rates per annum. This strong operational performance from the clear market leader confirms the stated intentions of an increasing number of Fortune 500 CIOs to shift more IT spending over to the public cloud at an accelerating pace.

- Operating margin ramp-up is vastly under-appreciated. Most of the Street is incorporating significant operational deleveraging assumptions or limited operating margin expansion forecasts for AWS over the next 5 years. My view is that long-term margins will be much higher due to a mix of 1) More muted IaaS pricing decline assumptions relative to expectations; I believe an attractive oligopoly industry structure will translate into pricing cuts being closer to 8%-10% annually on core IaaS computing and storage services instead of the 20%-30% implied by Moore’s Law, 2) A favourable sales mix-shift to faster-growing, higher-margin PaaS such as database application subscription services and most notably 3) Easily realizable benefits from massive economies of scale and fantastic incremental margins which should be much higher than current ~19% GAAP operating profit margins today. Due to its clear first-mover advantage and the massive entry barriers for this business, among the largest “hyper-scale” infrastructure cloud service providers, AWS is likely the only one that is currently profitable at a 25% consolidated segment operating income (CSOI) margins. The business is 10x bigger than the next 14 competitors combined in terms of computing capacity, and in terms of revenue, around 5x the size of the next largest competitor – Microsoft’s cloud computing business Azure. 5 years from now, I believe AWS’ operating margins could be closer to 40%-50%, with EBITDA margins ranging from 60%-65%.

- The retail segment’s normalized profitability remains misunderstood by the majority of investors. Investors appear myopically focussed on the lack of or limited profitability of Amazon’s 1st party (1P) retail business on what is suppose to be a more efficient retail model than traditional brick & mortars (B&M). On this issue a couple of things come to mind: 1) Continued investments in the fulfillment and distribution network are necessary to support a superior customer service offering which in tern leads to continued share gains in under-penetrated product categories within a gigantic TAM; In the US alone Walmart has retail sales of well over $300bn, which is massive compared to Amazon’s entire 1st party sales which will likely be under $100bn this year. The highly successful Costco-like retail playbook of sharing scale efficiencies with the customer results in a superior service and a more loyal and valuable customer base, completing the virtuous circle that propels the Amazon Flywheel. Customer service and pricing levels are probably the two most important competitive factors in mass market retailing, and I believe that these universal truths have been overlooked or under-appreciated by investors who study Amazon and arrive at the conclusion that Amazon can simply pass less value to their customers in order earn a higher profit over the short-term without risking erosion of its moat longer-term.[1] In short, I believe that Bezos’ strategy to densify Amazon’s fulfillment and distribution network, in time, will payoff hugely for shareholders and allow them to continue to crush the competition. Although I concede that Bezos might be excessively over-investing in some areas at rather low rates of return such as the Fire phone, I am confident that most of Amazon’s investment programs will be highly accretive over time. Ongoing initiatives such as Kiva Robotics, the Drone program, Prime Now, Prime Fresh, and content investments that support Prime’s subscription video-on-demand (SVOD) service are multi-billion dollar bets that are depressing current profitability. 2) The second thing and undeniable truth is the rapid growth of very high-margin 3rd party (3P) marketplace sales and a faster growing mix of 3P Gross Merchandise Value (GMV) vs. 1P, along with growth in Amazon Prime membership subscription fees and Fulfillment by Amazon (FBA) services for merchants. I estimate that Amazon’s 3P GMV will grow at 30%+ per annum, and these services are accelerating retail gross profits, expanding gross margins and further propel the Flywheel. Because of these additional services, Amazon is no longer destined to the financial shackles of being a pure low-margin, (although extremely efficient) 1P fulfillment-based retailer. Due to these large investment programs, along with the under-appreciated growth of these higher-margin services, the market has consistently and unfairly accused Amazon of being a low-margin retailer that barely generates any real profits.

Why does this opportunity exist?

Amazon broke out revenue and operating profit figures for its AWS division during its Q1 results this year, which revealed a very profitable cloud computing business. After being thought of as a loss-making division, by now AWS’ profitability is well known to most investors. This event, along with a steadily improving margin profile for the retail business has catalyzed a substantial re-rating of Amazon shares year-to-date.

However, I believe Amazon remains largely a misunderstood investment story. Most investors still under-appreciate the magnitude of the AWS opportunity as growth and margin forecasts appear far too low by most sell-side analysts. Bezos’ investment time horizon is longer than most investors, who typically under-price the long-term growth prospects of high-quality compounders. The market also typically does a bad job of valuing divergent cash flow streams such as, in this case, the Retail segment vs. the Public Cloud Infrastructure segment; Most analysts still have not woken up to the fact that AWS is a material value driver and consequently do not value Amazon as a sum-of-the-parts but instead assign a consolidated multiple as their main valuation framework. I believe this has led to grossly conservative implied valuations of AWS, which I believe will become a much more valuable franchise than the Retail business over time. As an industry, public cloud infrastructure services also has a limited reporting history, and investors have assumed that it is a very low-return, unprofitable business. Financial disclosure of hyper-scale cloud infrastructure providers such as AWS, Azure and Google Cloud remains quite limited as Azure and Google currently do not break out their cloud division financials. What’s more, publicly-traded companies with comparable economic characteristics to AWS are not obvious to the casual market observer, making it harder to value. Finally, there is a misunderstanding of Retail’s long-term earnings power due to the different growth initiatives within this segment such as Prime, FBA, and 3P which all have different growth and margin structures – and all at different points of their respective investment cycles – which mean lazy analysis will likely lead to a faulty investment conclusion.

AWS – The Fastest Growing Enterprise Technology Company in History

Brief Business Overview

AWS was formed in 2006 to sell excess cloud computing capacity unused mainly by the Amazon.com retail website. Providing cloud infrastructure services is largely a recurring, subscription-based business which can be further broken out into three main service lines: Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), and Software-as-a-Service (SaaS). IaaS is the provision of storage, computing power, virtualization and networking services over the cloud. PaaS is the provision of an operating system platform and related services over the cloud, and SaaS is the provision of application software such as Salesforce CRM, for example, over the cloud.

Source: Gartner: Magic Quadrant for Cloud Infrastructure as a Service, Worldwide report

AWS is the clear market leader and should be posting revenues of nearly $8bn this year and well above $12bn next year, making it the fastest growing enterprise technology company in history. For reference, Google is the only other technology company to achieve $10bn in revenues in less than 10 years!

Value Proposition

Similar to how households or enterprises can pay for electricity service from a local utility provider, customers can rent computing and storage units over the cloud from an infrastructure cloud service provider on a pay-as-you-go basis. Since companies already outsource their electricity requirements, there is little reason why IT infrastructure shouldn’t be commoditized over the cloud as well. The current shift to public cloud services is reminiscent of a time during the industrial revolution when companies started shifting their power consumption to electric utilities instead of generating their own power source in-house. WRT to alternative IT solutions, traditional IT outsourcing solutions provided by firms such as IBM or HP are typically more expensive, and on-premise solutions require large, upfront investments into in-house IT resources such as software, hardware and consulting services.

“No company that we [Andreessen Horowitz] invest in anymore actually ever

buys any hardware” – Marc Andreessen, TechCrunch, January 2013

The head of AWS, Andy Jassy, discussed several key reasons why companies are flocking to the cloud.[2]

- Cloud enables a service consumption model that transforms a customer’s fixed capex to variable cost.

- Due to superior capital efficiency, hyper-scalers such as AWS realize far more economies of scale than many enterprises could on their own. Hyper-scalers achieve superior asset utilization vs. customers that may have sub-20% data centre utilization rates in some cases.

- Cloud enables on-demand models to prevent over or under provisioning of storage and computing during peak or low demand periods.

- Companies can outsource IT infrastructure requirements and focus their resources on their core business.

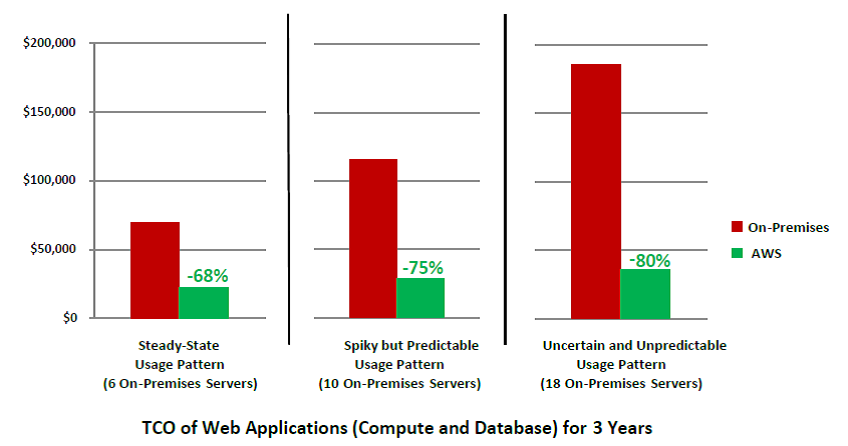

- Pricing is very attractive in comparison to legacy on-premise solutions. As shown below AWS has a huge pricing umbrella over traditional on-premise solutions with pricing for basic computing and storage services ranging from 68%-80% cheaper than comparable on-premise solutions.

Source: Gartner, Deutsche Bank

Because of these reasons and the increasing comfort around the security and reliability of hosting data over the public cloud, adoption is hitting a major inflection point according to CIO surveys. General Electric, for example, is a major customer of AWS and is planning to shut down 90% of their 32 data centers over the next five years.

The Moat – it’s very wide, and growing

Economies of scale act as a large entry-barrier as significant capex is required to break-even in this business. AWS truly is the 800-pound gorilla in this space with greater than 10x the computing capacity of the next 14 largest competitors combined. As a result, they are the only current existing player operating at scale. In addition, switching costs are also increasing over time as customers that migrate large data workloads over to a single cloud vender can easily get locked-in. Switching costs also increase as customers purchase incremental value-added services on top of AWS’ basic infrastructure services. One notable example of customer lock-in is Netflix, which relies on AWS for its entire IT infrastructure; Netflix has said that it would be a “significant multi-year effort to switch infrastructure cloud providers.” For AWS this is all great news as they have already reached a critical mass of 1 million plus sticky customers and operate a largely subscription-based business model that benefits from massive scale economies and high barriers to entry. Finally and most importantly, the business will also benefit from a massive network effect of 3rd party developers/software application vendors as customers will likely stick with only 1-2 cloud provider platforms with the largest breadth of IT services.

With respect to pricing, unlike what many investors believe, the business of providing public cloud infrastructure services is not a pure commodity-like business. Yes, at the basic core the business is about renting out uniform storage capacity and computing power units. But other competitive factors such as security, reliability, speed and a broad set of features are critical for large, sophisticated, enterprise-grade customers who are beginning to shift an increasing amount of mission-critical data to the public cloud. Some of AWS’ competitors with businesses tied to traditional on-premise solutions have argued that AWS is only suitable for start-ups and is not an “enterprise-grade” service. This is clearly not the case if we take a quick look at AWS’ customer base, which includes large enterprises such as General Electric, Comcast, Vodafone, Unilever and the CIA. The lucrative CIA contract was won by AWS over IBM Softlayer, despite Softlayer’s lower quote, because according to the CIA, AWS had a “superior technical solution”. If this is not the smoking gun that attests to AWS’ “enterprise-grade” quality, which helped the company win over a contract from an organization with one of the strictest security standards in the world, then I don’t know what is.

Attractive Industry Structure and Economics Developing

Gartner projects the IaaS market will be worth $17bn in 2015 and will double over the next 3 years. I believe Gartner’s CAGR’s estimates are too low and I have modelled an industry CAGR closer to 50% over the next five years. Why? Well, AWS’ compute and storage services’ usage rates are growing at 90%+ YoY, (Revenue is growing nearly 80% YoY) Microsoft recently disclosed that its Azure business is growing revenues 135% YoY, and Google Cloud is likely growing at triple-digits as well. So with the market leaders currently growing at 3x-4x the rate that Gartner projects, and with the industry conservatively at less than 5% of the TAM and rapidly growing due to a major multi-decade shift in IT spending, do we really think that industry growth will be just 30% per annum over the next few years? Even assuming 50% per annum growth over the next 5 years, the size of the cloud infrastructure market will still be ~13%-26% of the TAM, implying plenty of growth well beyond 2020.

In terms of competition, simply due to the massive economies of scale required, I see the majority of share in the IaaS market split between AWS, Microsoft Azure, and Google Cloud over the next several years. The current market setup is a 2-horse race between AWS and Azure, with Google at a distant third and not in the minds of most large enterprises. AWS has been steadily gaining market share and is now nearly 5x larger than Azure with a ~47% share; Azure will likely generate run-rate revenues of ~$1.6bn this year and according to my industry due diligence Google Cloud is likely a sub-$1bn business. The rest of the industry is mostly comprised of the traditional enterprise IT incumbents such as HP[3], IBM, and Oracle who have an incentive to protect their legacy businesses which will likely be cannibalized.[4] As a result, they emphasize more of a hybrid-cloud approach, and unlike Microsoft’s Nadella, were very late in the game in pursuing a “cloud-first” strategy. Due to the high entry barriers, these sub-scale players will likely operate a niche cloud business without any significant market presence. For reference, the Goldman Sachs analyst thinks that even Azure is likely operating on negative gross margins and is not expected to break even until the second half of 2016 or early 2017 despite being the clear #2 player with a $1.6bn business!

“While many companies are developing commercial cloud offerings, there are only two driving enterprise cloud platform innovation at massive scale: Amazon and Microsoft.” – Microsoft CEO Satya Nadella, Microsoft Q1 2016 Conference Call

There appears to be some sort of consensus that, longer-term, the market will eventually develop into a duopoly between AWS and Azure. Although a possibility, I have to disagree. I think Google is currently being underestimated and could potentially be a very large player in this space. I believe Google’s limited traction thus far in the cloud infrastructure market has largely been 1) a lack of focus, especially in developing a rich feature set such as the one available on AWS, 2) very limited marketing to enterprises, and 3) limited time in market, as their cloud business only launched 2 years ago. The first issue shouldn’t be a problem for Google longer-term given their technical prowess. The recently announced hiring of VMware cofounder Diane Green to head Google’s Cloud business, to me, signals that Google is willing to tackle the enterprise market more aggressively.

Google’s 8th employee and SVP of technical infrastructure, Urs Holzle, recently stated that he thinks in 5 years Google’s Cloud business could be larger than its entire Search Advertising business! I think Google’s advertising business will likely top $100bn in revenue by 2020. So what he is basically saying is that Google Cloud will grow by over 100x in 5 years! For reference, I am only projecting AWS to grow to ~$54bn in revenues by 2020. At first I thought Mr. Holzle was being delusional. However, the more I thought about it the more I see a bit of truth in his statement. Although Google Cloud is subscale now, I believe the conditions are present for them to compete very effectively. Firstly, they likely have one of the largest existing datacentre footprints available that power their heavy-traffic, security-sensitive, consumer-oriented cloud apps such as YouTube, Google Maps, Drive, and Gmail; with that also comes the expertise required to host extremely large data sets. As such, because of their existing scale I believe they are likely already operating at gross margins higher than Azure, or at the very least have the infrastructure in place to scale up very quickly. Secondly, unlike the traditional IT incumbents, Google doesn’t have a highly profitable legacy business to protect, and they are willing to tolerate large losses for a long time in order to scale up. Obviously having a war chest of nearly $80bn also helps. Thirdly, unlike Azure but like AWS, Google intends to build its cloud OS platform with open source technologies. Similar to their rather successful strategy in mobile by using Android to develop an open ecosystem of 3rd party developers and customers, I believe this strategy will play out well in the cloud infrastructure world as well. The fact of the matter is that despite being able to work with other technologies, Azure’s cloud platform is built with very Microsoft-centric technologies, which is not friendly to the modern day developer who doesn’t code in the .NET Framework. Instead, Azure appears built for Microsoft’s existing enterprise customer base, which they hope to protect from AWS and Google. Finally, Mr. Holzle has said that only ~1% of total storage capacity in the world is on the public cloud (implying a more aggressive TAM estimate than my own), meaning that we are still on the 1st pitch of the first inning in this game. In my view, Google has plenty of time to catch up.

With that said, it’s difficult to imagine AWS not maintaining its current share or even increasing it over time as they far along in the learning curve, are considered the clear industry leader by enterprises with the most robust and sophisticated features, and already have the largest 3rd party marketplace of applications on their platform. To be conservative and due to potential volatile changes in market share within a hyper-growth market, I model for AWS a 5-year top-line CAGR in-line with the cloud IaaS industry.

With respect to industry pricing, prices for basic IT infrastructure services are largely driven by Moore’s Law.[5] AWS has cut its prices nearly 50 times for basic IaaS storage and compute offerings over the course of the past 6 years, and Azure and Google have cut prices in-line to keep up. Google announced deep pricing cuts in April 2014, thereby effectively resetting IaaS prices for the industry, stating that AWS was over-earning by not passing on the full Moore’s Law cost savings to customers. Google cited that public cloud infrastructure providers such as AWS and Azure were cutting IaaS prices closer to 6%-8% per annum, which is a sign that industry pricing was already starting to firm up in true duopoly fashion. Due to the risk of more competitive pricing – mainly from Google – I am modelling a conservative base case scenario of IaaS pricing falling by 10%-20% per annum, which should be roughly in line with hardware cost savings from Moore’s Law and scale efficiencies from increased bargaining power. I believe the risk of a pricing war will decrease over time since share will mainly be allocated to a small handful of rational players. Azure has historically not been aggressive on pricing, and has a large installed base of customers to harvest cash flows from and to transition into the cloud. For Google, I believe their priority now is to dramatically improve their platform, such as launching additional features and services for their PaaS offering. I believe my industry pricing assumptions could potentially be a very conservative, especially if Google figures out that destroying the industry value pool alone will not win them share. The dream bull case would be if Google fails to gain any real traction, and the market evolves into a duopoly/quasi-monopoly between Azure and AWS with AWS having a dominating 60%-70% market share; pricing power of course would be much stronger.

Expansion into Adjacent Markets and the OS Ecosystem/Network Effect

Although an important component of the AWS investment story, I believe that the market has largely overlooked AWS’ expansion into the adjacent PaaS market, which should lead to a stickier, higher-margin business profile for AWS and a wider moat over time. PaaS offerings are higher value-added than basic IT infrastructure services with better pricing power and terrific incremental margins. These services encompass areas such as the Internet of Things, Mobile, Big Data Analytics, Email, and Desktop Virtualization that make up the foundation of a modern operating system (OS) platform over the public cloud. I think everyone in the industry has now woken up to the fact that the PaaS layer will be the most important public cloud battleground of the future; however, few have a leading, profitable IaaS business such as AWS’ with the customer base to cross-sell into.

One notable example of AWS’ success in growing their PaaS platform is their recently launched Amazon Aurora service. Aurora is a MySQL-compatible database engine with 5x better performance than the typical MySQL database and at one-tenth the cost of high-end commercial database offerings. Barely 2 years old, Aurora is already a $1bn+ business growing 127% YoY and is actually the fastest growing service line in Amazon company history. The database market is one of the largest sub-segments of platform software at around $40bn and Gartner thinks that cloud database services can grow at 45% CAGRs over the next several years. Clearly, Aurora is stealing massive market share away from database incumbents Microsoft and Oracle who have the leading on-premise solutions in this space; my due diligence suggests that Oracle’s database cloud product is growing closer to under 40% per annum. Aurora’s success gives me great confidence that AWS has the capability to build a leading PaaS offering amongst incumbents who have been in this space for decades.

Due to the favourable mix-shift of a faster growing PaaS business with better pricing power than IaaS, I believe AWS’ operating profit margins have more upside risk than what the Street anticipates. However, there are no good comparable publicly-traded businesses that can give us a clue on how AWS’ long-term margins can potentially look like. For this issue, I have to give credit a brilliant friend of mine who pointed out to Intel’s PC division as perhaps a relevant comparable.[6] How are these two businesses similar? Well, Intel’s PC business is another Moore’s Law type of business with high fixed costs, it benefits from tremendous R&D scale efficiencies, and is a dominant market share leader in PC processors with an 80%+ share. For reference, Intel’s PC segment reported ~$35bn in revenues and generated 42% operating margins in 2014. With the exception of perhaps a larger enterprise sales force, I believe AWS’ IaaS business shares quite a similar financial profile to Intel’s now mature PC business. However, as I already noted, AWS’ expansion into PaaS offerings with higher contribution margins vs. its more commoditized IaaS offering should lead to even greater margin expansion over time. This leads me to believe that eventually AWS could become an even more profitable business than Intel’s PC division ever was.

Growing on the back of a vast installed base of customers, AWS’ cloud computing platform Elastic Beanstalk will likely have a massive ecosystem of 3rd party developers/software vendors; Intel never had this type of network effect advantage. But what other technology company had a similar advantage? Off the top of my head, one business I can think of that benefitted from a similar type of ecosystem and thus had an overwhelming market share lead was Microsoft’s Windows OS for PCs. This was a phenomenal business that sold pre-packaged software at 100% incremental margins into an enormous open-ended growth market which propelled Microsoft stock to be one of the most valuable companies in the world at the turn of the 21st century. Just like how Windows was the dominant OS of the PC era, and iOS and Android are the dominant OS of the Mobile era, my belief is that AWS will likely be among one of the very few dominant OS platforms of the public cloud era. Already having achieved a critical mass of having the largest marketplace of 3rd party application software for 1 million+ sticky customers, and the most robust set of features (over 1,000 features have been introduced since inception), and with a business multiple times the size of the rest of the industry, I do not think this prediction is unrealistic. Also worth noting is that AWS should be able to easily leverage its R&D scale efficiencies to expand even further up the cloud stack into higher-margin application software such as SaaS over time, which will further expand its TAM. This is additional free upside not baked into Street estimates in my view. Now I can clearly see why Bezos wrote that AWS is market-size unconstrained.

In summary, I think AWS’ long-term economics will look like something in between Intel’s PC division and Microsoft’s Windows OS for PCs when they were nearing a mature growth phase, but with the added benefit of having a much larger TAM, and possessing the best combination of competitive advantages a business can have in my view – the network effect and massive economies of scale. By 2020, I believe AWS can grow revenues closer to $54bn (much larger than Intel’s PC segment), and generate operating profit margins somewhere between 40%-50% and EBITDA margins north of 60%-65%.[7]

Retail Segment – The Bezos Flywheel

As mentioned in my thesis the growth of FBA, Amazon Prime and 3P marketplace sales should drive general margin expansion for the retail segment over time, and further propel Bezos’ flywheel. Some analysts have pointed to Amazon’s slowing reported retail sales growth, but fail to appreciate the fact that faster growing 3rd party sales understates total retail sales to an extent, due to the fact that this is a commission-based business that earns a take-rate off of 3P GMV. The more important driver here is the growth in 3P GMV, which should remain very strong; this is due to the Amazon customer wallet being relatively under-penetrated in certain areas such as apparel, along with a massive remaining growth runway in retail sales. For reference, total US retail sales was ~$4.53 trillion in 2013, and is likely growing at a nominal GDP-like rate. I estimate that Amazon’s total global GMV (including 1P and 3P) will still be less than $1 trillion by 2020.

3P Marketplace, Amazon Prime and FBA – Trying to Decipher the Genius of Bezos

Amazon Prime is a very high-quality, fast growing business that generates annuity-like, subscription-based revenue streams. Prime membership numbers aren’t disclosed, but estimates based on surveys suggest that there may be up to 60-80 million members worldwide. Prime members tend to make more frequent purchases on Amazon (up to 2x-3x more in value than non-members).

Initially I was quite skeptical of the launch of a SVOD service for Prime members due to the multi-billion dollar content investments necessary to build a compelling offering, but over time I have come to see the attractiveness of such a business. One strategy a Pay-TV distributor can use to differentiate itself from the competition is to have differentiated content. Traditional Pay-TV distributors have licensed rights to exclusive sports content in order to protect the Pay-TV bundle. Another type of content strategy that appears to provide differentiation for a cable network or SVOD is to invest in exclusive original content. Over the past several years, we have seen distributors such as AMC networks, Starz, and Netflix pursue a strategy of investing in exclusive original content to some success. Amazon is now pursuing a similar strategy by producing, for example, three new seasons of Top Gear that will be exclusive on Amazon Prime. I believe Amazon is probably spending a couple of billion dollars on content streaming rights and production presently, and this expense pool will likely peak at around $3-$5bn over the next few years. For reference, Amazon’s largest OTT competitor, Netflix, spent ~$3bn+ on content in 2014, and is expected to spend between $4bn – $5bn this year.[8]

I think the economics of producing content appear much more attractive when it is paired with a global SVOD distributor which has access to a global pool of potential subscribers. Perhaps this is the main reason why John Malone recently built an equity stake in Lions Gate: I could be wrong, but the end game thesis could be to unleash some synergies by leveraging Discovery and Starz’ brand equity and global base of customer relationships to eventually build a high-quality, global subscription-based streaming service. With Lions Gate’s existing content streaming library and scale in content production, this business is currently experiencing a positive tailwind of high-quality content being re-priced higher due to steadily growing incremental demand from OTT players who are experiencing rapid growth in global markets. Maybe the legend John Malone sees this same inflection point in the economics of content production assets. With that said, I see the economics for Amazon’s streaming service particularly attractive over time since Amazon already has a global customer base that they can leverage for Prime subscription growth. Some analysts forecast that Netflix can eventually reach 200 million subscribers globally. Given Amazon’s global presence, I don’t see why they can’t get there eventually. This business will eventually throw off great incremental margins once it reaches a critical mass, as largely fixed content expenses will be amortized over a growing base of Prime subscribers. Based on Netflix’s per-subscriber valuations, I am extremely bullish on this business.

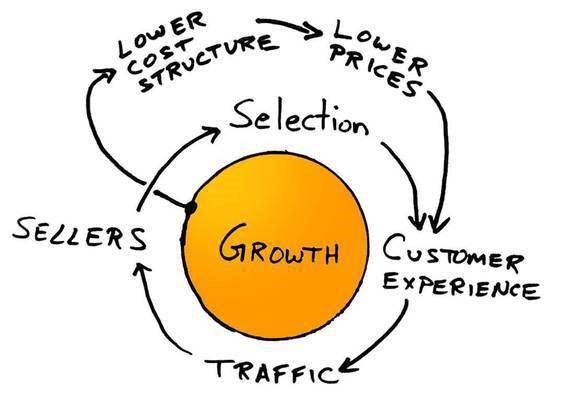

The genius of FBA is that it completes the virtuous cycle of more Prime eligible SKUs, better control of the customer experience, leveraging incremental fulfillment scale efficiencies, lower prices, and more Prime members. Long-term, this is superior model to e-commerce competitors who lack the breadth of SKUs and a high-quality, uniform customer experience. Credit to Andreessen Horowitz’ blog for this great image below which illustrates the Amazon Flywheel.

Source: A16Z Blog

Amazon reminds me of the successful Costco model of sharing scale efficiencies with customers, and maintaining a low mark-up pricing policy. The market consensus on Costco 10-20 years ago was that it was a low-margin retailer and expensive stock. Now the business is better understood as one of the most successful retailers in history.

Retail Segment Long-Term Economics

Quite detailed analysis is required in order to come up with an informed view of how consolidated margins may look like for the retail segment long-term. After discovering all these moving parts in the retail business which greatly complicates the story, it is no wonder that the sell-side has consistently for a long period of time under-estimated Amazon Retail’s margin upside.

Amazon’s Retail business can be separated into 1P and 3P sales. Because 3P sales (which are 100% gross margin) are based off a commission of 3P merchandise sold, I think the best way to think about how the retail segment’s long-term operating margins might evolve into is to start with Amazon’s GMV. GMV is an important metric for analyzing e-commerce models such as Amazon’s since the business derives total revenue from a mix of 1st party (1P) and 3P (marketplace) sales. Currently Amazon doesn’t disclose their GMV (what a surprise), but some analysts estimate that it might have been ~$180bn in 2014 or slightly 2x Amazon’s total retail sales. I believe this estimate is quite reasonable. If we assume that 60% of Retail’s GMV was 3P, and given Amazon’s take-rate of ~12% (this figure is based off of merchandise category), 2014 3P sales should be ~$13bn. Add $72bn for 1P sales and we arrive at around $85bn in total retail sales, which is around what reported Retail sales were for Amazon in 2014. There should also be a few billion of revenues in the mix from Prime subscription fees and FBA but for the sake of simplicity I will ignore these businesses for this analysis.

Now, let’s further split our analysis between North America (NA) and International. First off let me say that I am working on the general premise that Amazon has a much more efficient retail model compared to B&M, and current investments are obscuring the true profitability of this business. To summarize, items that are obscuring the “core” profitability of the retail business include R&D spending on the Drone program, investments in Kiva Robotics, the Fire Phone, TV and Tablet, Amazon Prime Now, Amazon Fresh, content streaming licenses and production, incrementally moving delivery services in-house and general growth investments into building additional fulfillment infrastructure closer to end markets. A few of these investments such as the Fire Phone may have a questionable return on investment profile, but I believe that most of these initiatives will turn out to be quite accretive to shareholder value. Ultimately, if you believe that Amazon doesn’t have a more efficient model than B&M, then I can’t help you here. For reference, the Bernstein internet analyst “gets it”, and has published an excellent note covering this topic.

North America 1P & 3P Operating Margins

For the more mature NA segment, if Amazon has a more efficient retail model, its 1P business should be able to earn operating profit margins higher than the most efficient B&M retailers at comparable sizes. I think Costco and Walmart are pretty good benchmarks. Costco is a $117bn business and generates ~3% operating margins; Walmart is a 5% operating margin business. From a product mix perspective, Amazon’s 1P gross margins are likely in the mid-teens, compared to Costco’s at around 10%-11%. Given what we know here, I’m confident that over time Amazon’s NA 1P business should be able to earn at least mid-single digit operating margins and potentially much higher. Note also that higher-margin categories such as CPG are still relatively under-penetrated by Amazon, and there should be a 1P sales mix-shift towards these categories.

In terms of GMV, the 3P business is likely growing much faster than 1P sales due to the growth of 3rd party merchants, FBA sellers and Prime users. By 2020, I estimate that 3P GMV could closer to 75% of total Retail GMV of ~$955bn or above $700bn. WRT the long-term 3P operating margin forecast, eBay’s marketplace segment is probably the best reference here. Despite eBay losing massive e-commerce share and underinvesting on its marketplace platform, it sports 30%+ EBIT margins with a GMV of $83bn in 2014. After taking into account payment processing expense differences from the PayPal segment, and differences between take rates (12-13% for Amazon vs. 8.5% for eBay), Amazon’s 3P operating margins should be conservatively at least ~30%-35% by 2020. I think this could potentially be a very conservative guess because I think eBay in general is not the most well-run business, and by 2020, Amazon’s NA 3P GMV should be at least multiple times larger than eBay’s GMV, providing much more scale efficiencies. Note that I am not adjusting for Amazon’s fulfillment expenses for 3rd party merchants here given that I am not sure what FBA’s contribution margins are. I would say that FBA strengthens the Bezos flywheel further and this business leverages scale efficiencies by utilizing fulfillment infrastructure that supports the 1P business. In addition, when the Kiva Robotics program is fully implemented, this initiative could easily lead to upside of a few hundred basis points of margin expansion which I am not capturing in my model.[9]

By 2020 I am modelling a 3P sales mix of 28% out of total retail sales. On that retail mix of 72%/28% of 1P/3P sales at 5%/30% operating margins, respectively, consolidated GAAP NA margins should be around low double-digits.

International

The largest criticism I have about this business is the company’s massive loses in China and the lack of any real traction in that market. Amazon entered China in 2004 and at one point not too long ago had the same amount of fulfillment space as JD.com (which I think is a pretty cheap stock btw). This is despite the fact that they currently have a 1% market share in direct-selling B2C marketplace sales compared to JD’s ~47% share. I think it’s time for an exit, and a sale of this business for an equity stake in JD.com could be the most attractive option at this point.

Within International Amazon has more mature businesses in markets such as the UK, France, Germany and Japan, and ones that are still subscale in China, India, Mexico, Spain and Italy. The growth opportunity in International remains enormous, but it will likely take a very long time before any large profits are realized. Thankfully, the International segment will likely remain a less valuable piece than NA for a very long time, and as such, is less of a key driver.

I am modelling 0%-5% GAAP EBIT margins for International by 2020, which I think prices in the risk of capitalizing losses permanently in failed markets such as China. When combined with low double-digit NA EBIT margins, Amazon Retail’s consolidated “core” operating profit margins should be within the HSD to LDD range by 2020. Note that this is still quite a rough guess and I have tried to be very conservative with my assumptions here, and have allowed some space in my analysis for potential low-return investments.[10] Due to the huge operating leverage in fulfillment, I see potential upside risk to this estimate.

Concerns – It’s all about the “Long-Term”

The most common argument I hear from the bears is something along the lines that Jeff Bezos is an empire builder who doesn’t care about profits or shareholder value.[11] Some also believe that Amazon is a de facto charity disguised as a for-profit company, run purely for the benefit of consumers at the expense of shareholders; I think this is almost akin to calling Amazon stock a Ponzi scheme. These are pretty ridiculous assertions in my view.

Is Jeff Bezos an empire builder? Probably. Does that make Amazon a bad investment? I don’t think so. When you are growing so quickly and reinvesting most of your profits in two of the largest markets in the world there is risk that you look like an empire builder and want to grow at any price. Bezos is obsessed about creative destruction and his investment time horizon of 5-10 years is longer than most CEOs and public market investors. In general his investment philosophy appears very flexible where he is willing to invest in lots of different projects where the risk/reward profiles range from substantial downside, but also a lot of upside optionality. When the inevitable failed project becomes apparent, the investment community are quick to scrutinize these low-returns.

In the grander scheme of things, I don’t believe a genius capital allocator has to head Amazon in order to make a lot of money here. Let’s take Amazon Prime for a quick example. If Amazon Prime raises its annual subscription price by 20% tomorrow, membership growth would likely remain very strong, implying that this would be a very wise decision in light of the goal to maximize shareholder value. Bezos won’t do this often, which might suggest that he is not a rational actor or shareholder friendly CEO. Perhaps this is the truth, yet I honestly think that this will eventually look like a rounding error in a DCF model. In my view, this is one case where the business is so wonderful it overrides the management factor in the investment thesis. I also think that critiques haven’t given Bezos enough credit for his successful investments and start-ups such as AWS.

For the record let’s take a brief look at some of Jeff Bezos’ capital allocation decisions:

-Acquired Twitch for around $1bn in 2014. Twitch is a hyper-growth, online live video streaming service with a niche audience. I think this media property has a very attractive platform for pursuing either an advertising heavy or subscription-based revenue model. In general I am quite bullish on the future of e-sports gaming and think this purchase could potentially be a home-run.

-Acquired Kiva Systems for $775 million in 2012. I think this was a pretty good investment as the Kiva robots can take out a lot of labour costs in Amazon’s fulfillment centers.

-Acquired Zappos for $1.2bn in 2009. All I know about this purchase is that Zappos was a very customer-centric shoe retailer that seemed pretty well-run and by 2008 was doing more than $1bn in GMV.

-Started AWS in 2006. I think this business alone makes up for all the losses and failed investments that Amazon will ever incur. If you own an asset that can be worth over $1 trillion within the next 10 years, I highly doubt you’re a value destroyer. The logic that Bezos doesn’t care about profits simply falls apart here when this business is at the cusp of one of the greatest technology growth cycles of our generation and is already reporting run-rate 19% GAAP operating profit margins. If Bezos is an irrational empire builder then why would he not operate AWS at 0% margins? Instead, industry prices for cloud infrastructure services are already firming up. So unless you think there are some serious sketchy accounting games going on here with the segment reporting, the “profitless forever” argument simply does not hold for AWS.

-The Fire phone has been an absolute disaster. In general it seems like Bezos’ strategy in consumer hardware is to sell products at a loss in order to drive incremental sales on the core retail platform.

-China has obviously been a disaster; nothing much needed to be said here. India, on the other hand, is a huge potential market and looks very promising.

-Amazon Now, AmazonFresh, Amazon Prime, and the Drone program. With the exception of Prime, these are all pretty large investment programs where the long-term pay-off may be questionable. Need a bit more time to judge these fairly.

Overall, I think his batting average is not perfect, but pretty damn good when you actually look at the record, and certainly better than most CEOs. Share dilution has also been quite limited over time. He writes that his job is to maximize long-term FCF per share in his shareholder letters. I just find it hard to believe that he is bullshitting in every letter just to trick shareholders into believing the Amazon story. It’s clear that Bezos thinks reinvesting all of Amazon’s profits into long-term projects is a more attractive use of capital then returning it to shareholders or reporting a healthy GAAP profit for Wall Street. What’s most important here is that Amazon’s earnings power has consistently increased over time, not what the company is reporting in GAAP profits.

Valuation – The Most Valuable Company in the World

On near-term valuation multiples, Amazon looks very expensive. It trades at ~42x 2016e EBIT[12] by my numbers, but this multiple will rapidly shrink in my outer projections years as AWS grows its profits significantly. By 2019 and 2020, backing out the Retail segment’s value, I believe we are getting the AWS business for 1x and -5x EBIT! On a fully consolidated basis, Amazon trades at just under 7x my 2020e EBIT projection. Even if we assign 0 value to the Retail business, we are paying 13.5x 2020e EBIT for AWS, which is still way too cheap in my view.

Base case, I am valuing the Retail segment on 20x 2020e EBIT, or ~$470bn ($961 per share), which translates into a GMV multiple of 0.5x. This is a large discount compared to Amazon’s historical GMV trading multiples of between 0.8x-1.0x, but reasonable I think, given the more mature future growth profile. For reference, large-scale US-based retailers with slower growth and without a high-margin marketplace business have typically traded between 0.6x-1.0x GMV. Worst case scenario, in 5 years this segment should be worth at least the current market-cap today.

I feel AWS deserves a higher multiple than Retail, and I am valuing this business at 25x 2020e EBIT or ~$600bn ($1,240 per share or nearly 2x Amazon’s entire current market-cap). This translates into ~11x 2020e sales and ~19x 2020e EBITDA. These multiples may look aggressive but I believe are well justified. Post-2020, AWS will still likely grow operating profits at 20%-30% per annum or higher on the back of massive ongoing cloud services growth. The business will also throw off increasingly predictable cash flow streams as enterprises are locked-in to a single cloud platform provider with most of their mission-critical IT workloads. Benefitting from a long-term secular industry tailwind, the business is also relatively non-cyclical; in fact I think it will be quite recession resilient and perhaps even counter-cyclical as enterprises have a greater incentive to cut costs by moving workloads over to the public cloud during a recession. If we take publicly-traded enterprise horizontal SaaS venders with near-infinite growth horizons as a set of comparables, I think AWS is a much better business than most of these names that trade at 8x-11x forward revenues with non-existent earnings, greater competition, lower switching costs, and smaller TAMs.

With the addition of the total incremental FCF and working capital that will be generated over the next 4 years, I think Amazon shares are worth between $2,000 – $2,350 by 2020 which should provide a 4-year annually compounded internal rate of return of 31%-37%. Worst case scenario, I think the stock trades at 19x my consolidated 2020e bear case operating profit numbers, which means shares are still worth $1,300 or 94% higher than where it trades today. This gives us about a mid-teens IRR. The stock would have to trade at a sub-10x 2020e EBIT multiple in order to be worth less than where it is today. This seems like a pretty good risk/reward.

The Bigger Picture: My Margin of Safety in Quality & Growth

Stepping back a bit, my former blog mate predicted here that Alibaba will become the most valuable company in the world in 10 years. I’d have to respectfully disagree with him. 7 to 10 years from now AWS alone could be worth well over a trillion dollars[13] and I’d bet that Amazon will be the first company with a trillion dollar market-cap. I love high-quality compounders with near-infinite/open ended growth horizons that are evolving into monopoly-like businesses, and I think the chances of me being wrong on both the prospects of AWS and Retail is much smaller than me being independently wrong on either one of them.[14] As such, I feel comfortable with the probability that either one of these businesses can more than justify the entire Amazon market-cap today, giving me my desired margin of safety.

Catalysts – Warning: Long-Term Time Horizon Required[iii]

I do not think this is a great holding for traditional hedge fund-like strategies that focus on shorter-term, event-driven trading opportunities. But make no mistake, I believe the timing for this investment is generally good and my suspicion is that AWS will continue to blow away Street consensus over the next several quarters. Therefore, I think the stock will continue to re-rate as growth-oriented investors pile in.

Catalysts may include:

- Additional AWS financial disclosure such as volume, pricing, cost structure and PaaS and SaaS business lines; A spin-off of AWS since there are virtually no synergies with the Retail segment (this move would be very unlikely, since Bezos would likely lose control); I believe if this segment were to be spun out today, shares could trade 50%+ higher. I would be very impressed with Bezos if he did this.

- Retail consolidated operating margin expansion from mix-shift to faster growing 3P operating profits, Prime subscription fees, current heavy investment phase rolling-off and greater operating leverage from fulfillment.

- Time: “The indefinite continued progress of existence and events in the past, present, and future regarded as a whole”.

Epilogue

In general studying Amazon was a very challenging and intellectually stimulating exercise. What I love about this idea is that it isn’t a hedge fund hotel or a consensus trade. I still think there are a lot of skeptics out there that love to hate the stock and criticize the lack of reported profits. I would not be surprised to receive a lot of push back from my readership base this time, even from the well-informed, very smart crowd.

Other potential ways to play the public cloud computing megatrend:

- Alphabet/Google: Could be an interesting backdoor play on the public cloud if their business begins to take off. Not a guarantee but I don’t think this is priced in at all.

- Microsoft: Thinking about this company makes me bored. But in all seriousness I think they will do OK.

- Chinese Internet Companies: According to some sources Alibaba’s IaaS has 1.4 million customers. Other major Chinese internet firms such as Baidu, JD, or Tencent may eventually get into this space.

- Short IBM/Oracle:

IBM is again on its death bed, and has to reinvent itself in order to remain relevant. Honestly I think their business is going to shrink a lot, and I don’t think there’s room for another major IaaS/PaaS player in the market. Commoditization of IT services is going to absolutely kill them. No one’s going to use their consultants or outsource their IT infrastructure to these guys if they can do it on the public cloud for much cheaper with a superior technical service. Even industries with tons of customer and regulatory sensitive data such as the Public sector, Financials, Insurance and Healthcare will all eventually move the vast majority of their IT workloads to the Public Cloud.

Oracle is another potentially interesting short. The issue for these guys isn’t that they won’t successfully transition into a cloud vender, but that it’s a much less profitable business than on-premise. When you earn 95% gross margins on your application maintenance fee streams and have to replace those with SaaS subscription fees at closer to 60%-70% gross margins, your business is going to get hurt. Also it appears that Amazon Aurora is gaining much more traction in the market compared to Oracle’s existing cloud database service.

[1] I think people under-estimate how price-sensitive consumers are to purchasing commoditized products

[2] Personally, after developing a web application myself, I know it would have been extremely inconvenient, very slow and more costly to purchase the servers to host my app over the internet instead of using a public cloud provider such as AWS.

[3] In fact, HP has already given up its Cloud Helion business and has recently announced a new partnership with Microsoft

[4] Just like how the Salesforces and Workdays of the world continue to disrupt the application software market, I see the same phenomenon playing out in the infrastructure services world

[5] Between October 2013 and December 2014, Amazon’s average monthly cost per GB RAM fell from $42 to $25, while Google’s dropped from $52 to $32. Increased bargaining power with hardware suppliers could also mean lower capex per unit going forward.

[6] Sometimes we have to use our imaginations to produce great analysis

[7] Assuming maintenance capex in the mid-teens

[8] I am a large bull on Netflix’ prospects as well but have not been able to find an attractive entry-point.

[9] Kiva Robots are estimated to replace 1.5 human workers in fulfillment centers and cost $25k a piece with an economic life of roughly 5 years

[10] My thesis is also not based on a bet that current large investments will roll-off by 2020, and thus margins will lift-off and shares will see a re-rating. I am just trying to come up with an educated guess about how margins may look like if we back out these investments by 2020. I am all for value accretive investments if they present themselves and if they are the best use of capital. So reported GAAP EBIT margins may never reach this EBIT margin range this decade, which is OK with me as long as I’m confident that capital is being allocated wisely. Honestly Amazon’s Retail business was one of the most difficult businesses I’ve ever analyzed, and I’ve never been a proponent of using precise calculations to drive an investment thesis/valuation.

[11] Amazon in fact recorded GAAP operating margins in the MSD during the mid-2,000’s

[12] I believe operating income will be the key driver of shares going forward. Street tends to focus on CSOI. I focus on GAAP EBIT because I think stock-based comp should be capitalized going forward

[13] Just assume 50% share in a TAM of $500bn and 40% operating margins = annual operating profits of $100bn; A modest 10x multiple would mean a $1 trillion dollar valuation!

[14] Risk is increased if you don’t know what you are doing.

[i] As a side note, part of the reason why I believe excessive diversification is overrated is because the intrinsic value of certain stocks held in a concentrated portfolio are the summation of multiple businesses that are potentially diverse across customer base, geography and product lines etc. Of course, certain single-stock/idiosyncratic risks still apply, such as value destructive capital allocation.

[ii] which comprises of spending on hardware, software, and services across the entire software stack

[iii] And when I mean “long-term” I mean 5-10 years!

very interesting and comprehensive – thanks for the food for thought

very detailed analysis, thanks!!

Very insightful post. Curious about your thoughts on why Warren buffet is doubling down on his bet on IBM despite deteriating prospect of this company?

I don’t know. Maybe 10 years from now he thinks earnings power will be higher.

Any comment on this counter-argument on Amazon?

http://www.gurufocus.com/news/386375/why-i-bought-walmart-over-amazon-

[…] holding a large amount of something like Berkshire Hathaway and a few technology disruptors like Amazon and […]